I learn so much from our government customers and governance experts. Attendees at the 2019 FreeBalance International Steering Committee (FISC) saw me typing furiously to take notes (and to tweet). Senior public servants, nominated by their governments, shared observations about Finance Ministry modernization. This included lessons from other countries articulated during workshops and discussions.

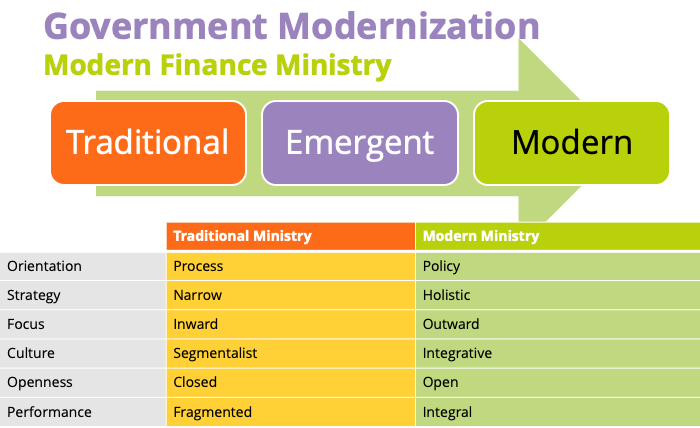

Most countries are on the journey from traditional through emergent to modern Finance Ministries. 12 dimensions of modernization were discussed in detail. Our customers were able to flesh out other modernization signs

How do traditional and modern Finance Ministries approach public finance management?

- From not using, or limited use of standard financial management diagnostics tools

- From donor-led reform (with characteristically high transaction costs)

- TO country-led reform driving development partner contributions

- From Ministry focus on managing revenue, expenditures and debt only to

- TO identifying how to improve the economic value add for citizens and businesses through government services

- From too many public finance and economic interventions to achieve effectiveness

- TO a focused set of government interventions to improve prosperity

- From lack of visibility into revenue, debt, state-owned enterprises, or sub-national governments

- TO comprehensive and timely visibility to all government financial matters with consolidated reporting

- From PFM practices as ceremony

- TO PFM practices designed to improve Ministry effectiveness

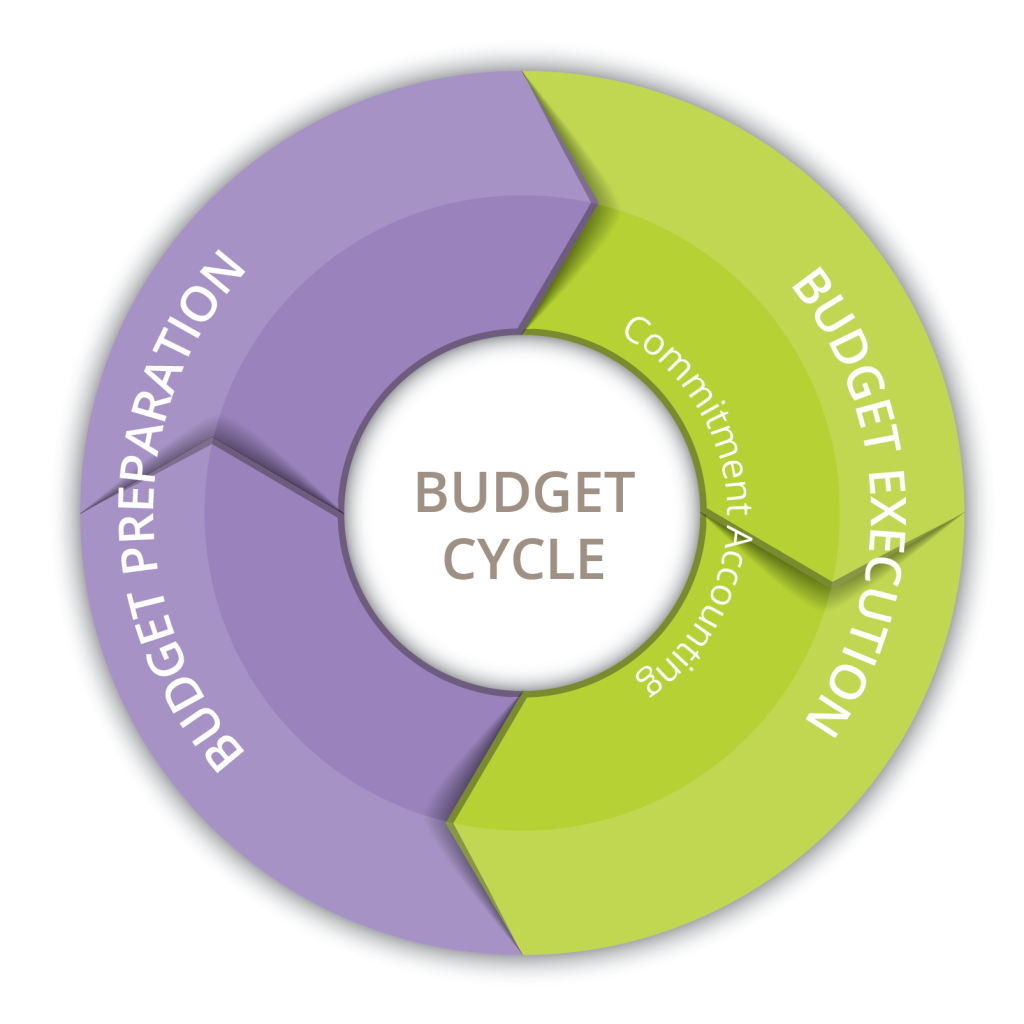

How do traditional and modern budget planning processes differ?

- From non-strategic budget planning, typically annual incremental budgeting

- TO strategic planning with scenarios and forecasts

- From organizational structure budgeting with limited alignment to national goals

- TO program-based and results-based budgeting tied to national goals

- From annual budget focus with limited modelling of multiple year initiatives

- TO full medium term approach including MTEFs

- From numerous political budget insertions including pork barrel spending initiatives

- TO strict fiscal rules including use of fiscal councils

- From budget approved months into the fiscal year, or never (as with continuing resolutions in the United States)

- TO efficient budget processes following the budget calendar

- From lack of credible budgets resulting in overspending and arrears, poor revenue and spending predictability, with need for supplemental budgets

- TO leveraging trend information, scenario planning and cost drivers for high predictability

- From separate and unrelated budget and accounting classifications

- TO a single consolidated Chart of Accounts for budgeting and accounting classifications

- From separate capital, operating, development, and salary budgets

- TO integrated budgeting including alignment with debt planning

How do traditional and modern budget executions processes differ?

- From line-item budget controls centrally controlled by Finance Ministries

- TO aggregate budget controls decentralized to line ministries

- From poor debt and cash sustainability

- TO effective liquidity management

- From poor cash management and support for hundreds of bank accounts, mostly controlled by line ministries

- TO full use of the Treasury Single Account to improve cash availability and liquidity

- From inefficient spending because of manual processes leading to underspending budgets

- TO efficient spending through automation

- From limited fiscal transparency

- TO timely fiscal transparency, including audit publication

- From underfunded audit departments focused on compliance

- TO well-funded audit departments focused on performance to improve effectiveness

- From inefficient government procurement processes

- TO effective procurement processes through automation and transparency, including increasing numbers of competitors to reduce costs, and supporting spend management programs

- From value criteria unrelated to national goals in procurement, or skewed to lowest price

- TO value for money criterial in procurement tied to national goals

- From uncompetitive tenders where governments pay higher prices than businesses

- TO highly-competitive government procurement with many bidders, complemented by processes to encourage local companies

What are the characteristics of traditional and modern government human resources?

- From few promotions with frequent hiring of outsiders to fill senior positions

- TO actively promoting public servants through talent management and capacity building programs including subsidizing education

- From using contractors to fill operational roles

- TO leveraging contractors for advice, mentoring and capacity building (including making capacity building part of contracts)

- From high turnover among public servants

- TO where public servants build careers in government

- From many unfilled positions

- TO a fully-staffed public service

- From the government as the employer of last resort

- TO government as the preferred employer, and the public service perceived as contributing to society