How does the government domain change the nature of the balanced scorecard?

Performance management has become an important trend in government organizations.

“It seems logical to expect high-performance measurement cultures in a sector that controls over a third of the economy.” (Jones, 2014)

A previous post made the case for the use of the balanced scorecard method for government performance management. This approach can help public sector institutions to simplify the complexities of performance management that, unlike the private sector, does not have an objective “bottom line” like profit. The methodology calls for the balance between financial, customer, internal progress and learning perspectives.

What is a Balanced Scorecard in Government?

The balanced scorecard methodology was originally developed for the private sector, but its potential to improve government performance is even greater. Given the fundamental differences between public and private sector management, this post looks at emerging good practices in public sector balanced scorecard implementations and the various balanced scorecard components. This includes structural adjustments to the balanced scorecard in government rather than organizational change management practices.

The reason we refer to “good practices” rather than “best practices” is because it depends on the context. Quite frequently, so-called “best practices” are too complicated or unnecessary in many government organizations.

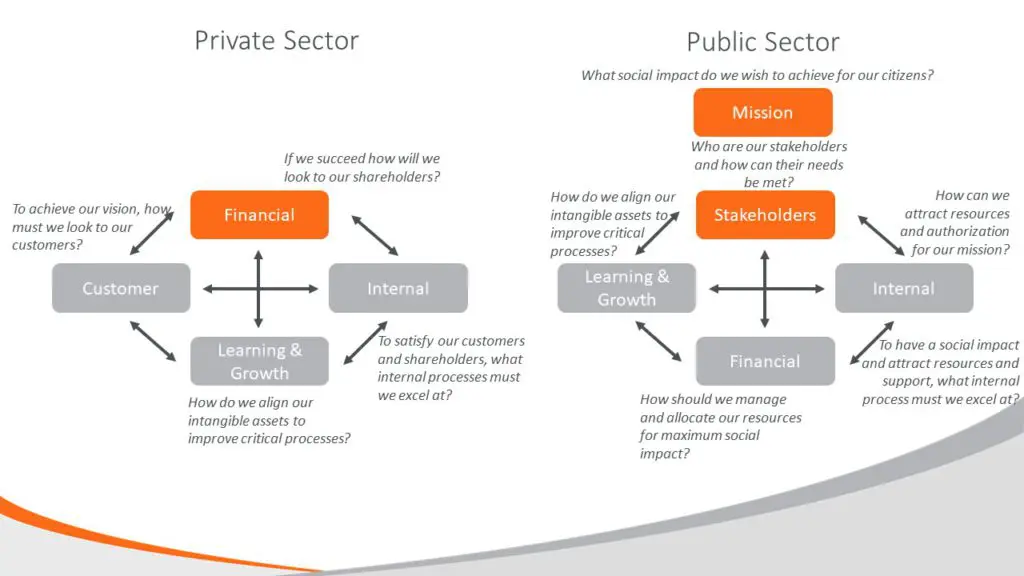

Differences Between Private and Public Sector Balanced Scorecards

There are four fundamental differences in the structure of public sector and private sector balanced scorecards:

- Mission Alignment

- Budget Alignment

- Customer Perspective

- Financial Perspective

What then are the elements of a balanced scorecard for public sector organizations?

1. Mission Alignment

Mission and mandate must move to the top of the balanced scorecard for government structures.

Mission and mandate statements can be important in businesses, but the traditional balanced scorecard in the private sector places financial perspectives at the top. This is not relevant in government where there are no shareholders. The raison d’être of a government is the social impact it makes – its mission.

2. Budget Alignment

Government budgets must adjust to balanced scorecard insights and results.

Budgets are legal documents in governments but only guidelines in a business. Any performance management system in government must therefor be aligned to budget allocations. The “Balanced Scorecard provides an excellent opportunity to tie resource allocation and strategy. The human and financial resources necessary to achieve Scorecard targets should form the basis for the development of the annual budgeting process. (Niven, 2008)”

3. Customer Perspective

The notion of the “customer perspective” must change in the government balanced scorecard to reflect the reality of stakeholders that could differ based on mission.

The traditional balanced scorecard has the “customer perspective”. This is often changed because the concept of citizen is customer is an “inappropriate metaphor” that over simplifies the relationship between the government and its citizenry. This perspective is often renamed as “citizen” perspective or “stakeholder” perspective and moved to the top of the template to highlight the key stakeholder deliverables and outcomes.

4. Financial Perspective

The financial perspective, including budgets, must be considered as the prime enabler of government performance, not the end result, or bottom line.

The financial perspective is the top concept in the private sector, but not in government. As the academics have pointed out:

- For a government agency, financial measures are not the relevant indicators of whether the agency is delivering on the rationale for its existence (Kaplan, 1999)

- The financial consideration can play an enabling or constraining role, but rarely as the primary objective. (Chai 2009)

This moves the “financial perspective to the bottom of the template. The overall objective of most public sector, government and not-for-profit organizations is not to maximize profits and shareholder returns. Instead, money and infrastructure are important resources that have to be managed as effectively and efficiently as possible to deliver the strategic objectives. (Marr, 2008)”

Alternative Views

Customer Perspective

The notion of the “customer perspective” should change in the government balanced scorecard to reflect the reality of stakeholders that could differ based on mission.

Some observers argue that citizen, business and other stakeholders are effectively government customers (Kaplan, 1999; Niven, 2008; Parmenter 2012). Others (Marr, 2008; Whittaker, 2003) take the view that there are many more stakeholders in government than businesses.

“The stakeholder perspective is arguably the most important one for government agencies because achieving a mission does not necessarily equate to fiscal responsibility. The organization must determine whom it serves and how their requirements can best be met. This perspective captures the ability of the organization to provide quality goods and services, effective delivery, and overall stakeholder satisfaction. (Whittaker, 2003)”

Yet, others take the view that the “customer perspective” ought to be renamed as the “citizen perspective” because citizens are the ultimate stakeholders in government. Much of the literature from practitioners, anecdotally, takes this view.

Additional Perspectives

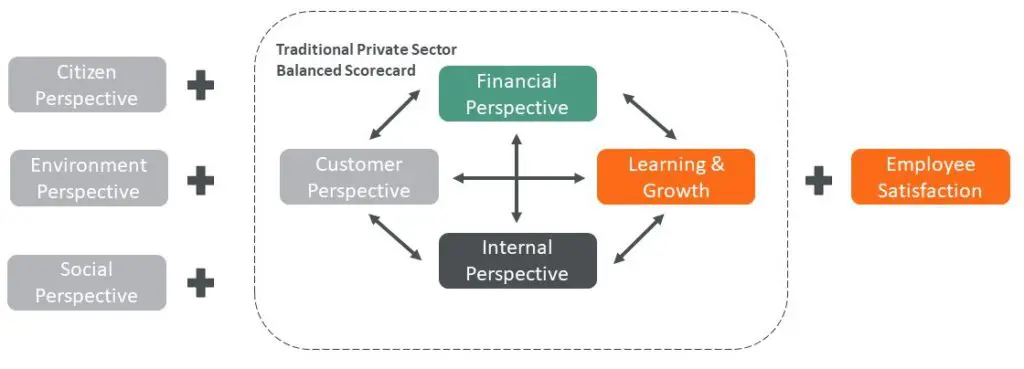

The addition of new perspectives are prescribed based on the context for performance management. The Sustainable Development Goals justify the addition of new perspectives.

The nature of government performance may justify the inclusion of additional balanced scorecard perspectives. For example, the notion of employee satisfaction, which some argue “is far too important to be relegated to a subsection within internal process” (Parmenter, 2012).

Many argue that the notion of stakeholders needs to extend to community and environment (Parmenter, 2012). This could be extended to even more perspectives when the Sustainable Development Goals are considered:

- Economic growth: Society’s wellbeing would be maximized and poverty eradicated through the optimal and efficient use of natural resources. Particularly, the overriding priority should be given to the basic needs of the world’s poor people.

- Social equity: This component refers to the relationship between nature and human beings, uplifting the welfare of people, improving access to basic health and education services, fulfilling minimum standards of security and respect for human rights, too.

- Environmental protection: It is concerned with the conservation and enhancement of the physical and biological resource base and eco-systems.

- Chai, 2009

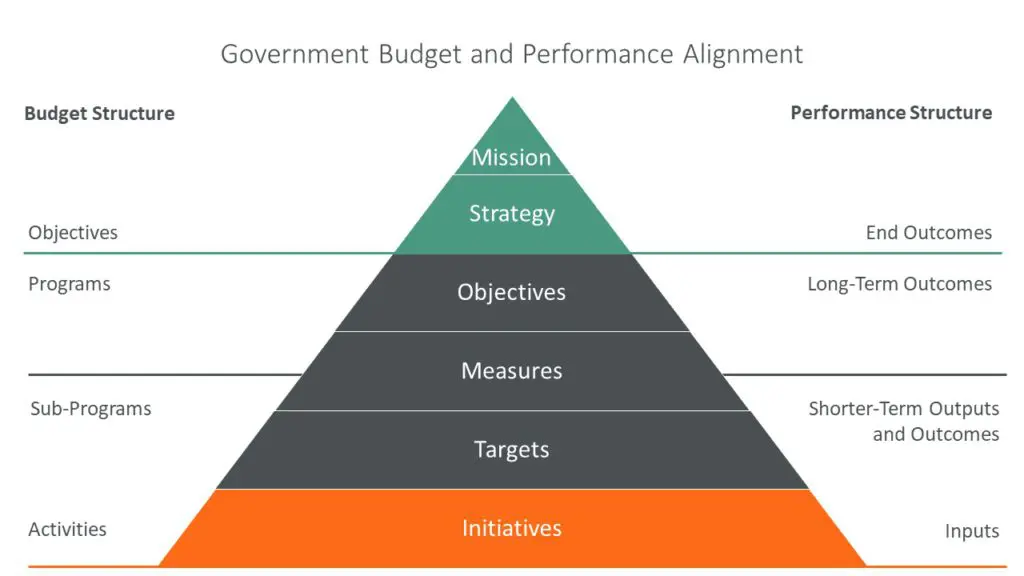

Cascading Measurements

Balanced scorecard measurements should be organizationally aligned in government. These measurements should be relevant while not overburdening organizational units.

The balanced scorecard is used in very large organizations to cascade measurements. However, given the complexity of government this could result in government organizational units becoming overburdened with measurements and public servants ending up with personal scorecards that have no relevance with the government’s mission.

Cause and Effect

Cause and effect concepts are useful in government balanced scorecard to test linkages between outputs and outcomes.

The balanced scorecard technique leverages “strategy maps” and other techniques to illustrate the cause and effect connections among perspectives. This approach is thought to enable better resource allocation and align outputs with outcomes.

Take Outs

- The public sector is different, requiring changes in perspective and structure

- Not all good practices from the private sector are appropriate

- Context determines approach based on government size, tiers, level of development

- Overly complex systems defeats the purpose of the balanced scorecard to focus on what’s important

References

- Chai, N. Sustainability Performance Evaluation System in Government, A Balanced Scorecard Approach Towards Sustainable Development. Springer, 2009. http://www.springer.com/us/book/9789048130115

- Jones, S. Impact and Excellence, Data-Driven Strategies for Aligning Mission, Culture, and Performance in Noprofit and Government Organizations. Jossey-Bass, 2014. http://www.wiley.com/WileyCDA/WileyTitle/productCd-1118911113.html

- Kaplan, R. The Balanced Scorecard for Public-Sector Organizations. Harvard Business Review, 1999. http://www.fetp.edu.vn/attachment.aspx?ID=43073

- Marr, B. Managing and Delivering Performance, How government, public sector and not-for-profit organizations can measure and manage what really matters. Butterworth-Heinemann, 2008. http://www.sciencedirect.com/science/book/9780750687102

- Niven, P. Balanced Scorecard Step-by-Step for Government Nonprofit Agencies. Wiley, Second Edition, 2008. http://www.wiley.com/WileyCDA/WileyTitle/productCd-0470180021.html

- Nurcahyo, R; Wibowo, A; Putra, R. Key Performance Indicators Development for Government Agency. International Journal of Technology, September 2015. http://www.ijtech.eng.ui.ac.id/index.php/journal/article/view/1840

- Parmenter, D. Key Performance Indicators for Government and Non Profit Agencies. Wiley, 2012. http://www.wiley.com/WileyCDA/WileyTitle/productCd-1118235304.html

- Whittaker, J. Strategy and Performance Management in the Government. Pilot Software, November 2003. http://www.exinfm.com/workshop_files/strategy_pm_gov.pdf