Why Governments Should Use The Balanced Scorecard

Governments around the world have implemented various performance management concepts. These are often known as results-based management or performance budgeting. However, there have been mixed results for government performance management initiatives.

“Current systems for measuring performance in the public sector present some limitations because they are based only on efficiency, effectiveness and economy indicators, which are mainly financial that fail to measure the fulfilment of environmental and social objectives of the public organizations.” (Mihaiu, 2014)

Originally developed to overcome performance measurement challenges in business, the balanced scorecard is highly relevant to the public sector. The “balanced” notion of the balanced scorecard that combines financial, customer, internal process, learning and growth perspectives provides a holistic performance framework. This approach can overcome many of the difficulties associated with understanding and implementing performance management in government. It is through the exercise of balancing performance needs that makes the balanced scorecard compelling for government and other public sector organizations.

“A properly constructed scorecard is balanced between short- and long-term measures; balanced between financial and non-financial measures; and balanced between internal and external performance perspectives. The scorecard is a management system that can be used as the central organising framework for key managerial processes.”

(Mackie, 2008)

What Is The Balanced Scorecard?

Corporate, or business, performance management is complicated and many businesses fail to improve performance. Others impose performance measures that generate perverse incentives. The balanced scorecard methodology is designed to overcome many of the challenges in developing performance management systems by aligning performance incentives with organizational strategy.

The balanced scorecard examines performance from four perspectives:

- Learning and Growth

- Business Process

- Customer

- Financial

An effective balanced scorecard exercise will result in a simple structure that focuses decision-making on what is organizationally important.

What Are The Benefits Of The Balanced Scorecard?

The balanced scorecard provides governments with a more holistic performance management methodology. Important differences in the public sector include the replacement of customer perspective with citizen perspective which is the ultimate ‘result’ rather than the financial perspective used in the private sector.

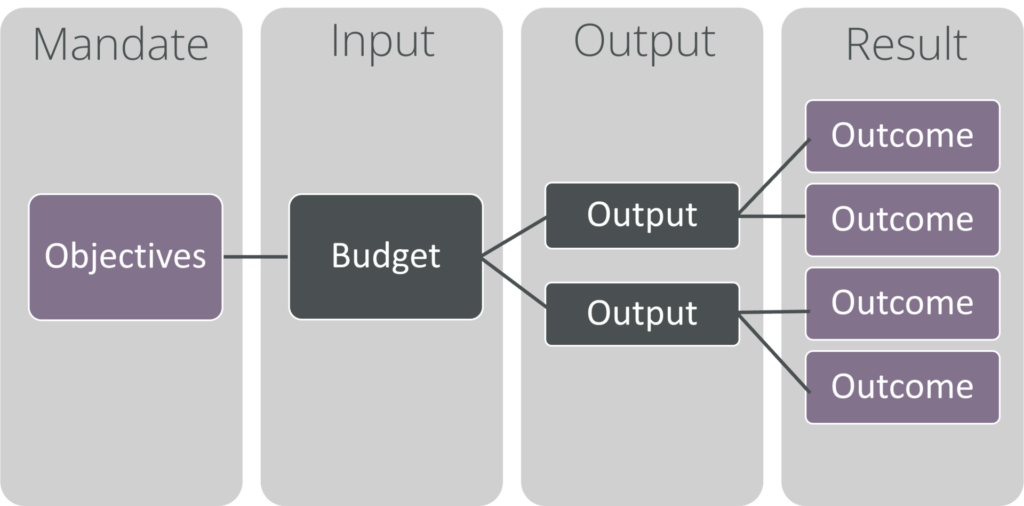

Alignment of Budget to National Objectives

The lack of a bottom line in Public Financial Management makes outcomes much more difficult to validate. Furthermore, politics often drives input-focused decisions (i.e. spend on projects in the politician’s district).

The balanced scorecard helps governments align outputs to outcomes and national objectives. This enables governments to select and test outcome measurements.

Alignment of Goals to Strategy

Businesses operate fewer “lines of business” than governments which creates issues of both scope and scale and makes whole-of-government performance management difficult:

- Scope: Budgets must be tied to performance because governments run commitment accounting

- Scale: Cascading complex objectives through MDAs and divisions to individual public servants is complex because there are so many staff members

Departmental and program related performance can also be challenging which can create information overload – there are simply too many possible measures.

Another issue is that public sector organizations are budget driven.

“As compared to commercial institutions, government agencies face a unique set of challenges when trying to manage performance and achieve their strategic goals and initiatives. Their mission and budgets are often decided externally… Additionally, agencies face the uphill task of meeting their goals without direct control of shrinking budgets and resources. This furthers the need for managing performance at every step along the way. ”

(Whittaker, 2003)

The balanced scorecard enables governments to align ministry, departmental, agency and personal goals with strategy. This eliminates many potential performance indicators that are not material to meeting government goals.

Ability to Add Context to Performance

Businesses operate within well-understood domains. Outcomes that drive profit are also well-understood. Public sector performance or results-based systems suffer from practical measurement problems as in many cases the outcomes are difficult to measure directly. This makes it difficult to identify outcomes that are relevant to government strategy.

Governments also have a more complicated performance lifecycle than the private sector because of the link to the budget process and the need for transparency.

The balanced scorecard enables government organizations to add context to performance results. Extraordinary events can be described with impacts to outputs and outcomes described.

Accountability Incentives

Businesses often offer significant performance incentives to employees. However, in government incentives that are tied to outcomes are difficult. Government organizations are typically managed based on compliance to statutory and budget rules. The introduction of management by outcomes can generate a fear of unintended consequences.

The balanced scorecard enables governments to better communicate goals for performance alignment. The exercise of developing and implementing a balanced scorecard, when accomplished properly, acts as the nexus for organizational change management.

Conclusion

The balanced scorecard enables tying long-term government goals to annual and medium-term budget proposals which improves program evaluation. The balanced scorecard is also an effective transparency mechanism as it provides evidence of progress towards goals and validates policy.

References

Diamond, J. Establishing a Performance Management Framework for Government. Presupuesto y Gasto Público, May 2005

Kamensky, J. Performance Measurement: 3 Challenges Every Government Faces. GovExec, November 27, 2012

Kaplan, R. The Balanced Scorecard for Public-Sector Organizations. Harvard Business Review, 1999

Kaplan, R. Conceptual Foundations of the Balanced Scorecard. Harvard Business School Working Paper, 2010

Mackie B. Organisational Performance Management in a Government Context: A Literature Review. Mackie Public Management, 2008 http://www.focusintl.com/RBM064-0064768.pdf

Mayne, J. Challenges and Lessons in Implementing Results-Based Management. Sage Publications, 2007

Mihaiu, D. Measuring Performance in the Public Sector: Between Necessity and Difficulty. Studies in Business and Economics, 2014 http://eccsf.ulbsibiu.ro/articole/vol92/925mihaiu.pdf

Whittaker, J. Strategy and Performance Management in the Government. Pilot Software, November 2003