Also, why are there many “spending reviews” in developed countries?

Why can’t advanced economy governments leverage program and performance structures to:

- rapidly respond to spending needs during fiscal shocks like pandemics and economic crises?

- easily adjust spending priorities based on actual performance?

- quickly reorient spending priorities based on political promises made by new governments in power?

Context: this is a critique of G7 & OECD country public finance response to follow government priorities

- It’s nothing to do with political dogma, it’s about leveraging good Public Financial Management (PFM) practices to support government priorities

Consider the pandemic response: what’s the reallocation mystery? Shouldn’t reallocation be a simple technical adaptation? Advanced economy governments seem to support most of the pre-requisites:

- program budgeting

- results-based budgeting

- business case frameworks

- accrual accounting (mostly modified accrual)

Yet, many of these countries seem ill-prepared to quickly re-allocate funds to target the crisis

- or, flexibility re-allocate as new information is made available

Interestingly, the first year of Program Assessment Rating Tool used in the American Federal government found that 50% of programs were classified “results not demonstrated“

An alternative view: effective budget reallocation and rapid procurement leveraging effective PFM systems has been drowned in the over-politicized pandemic politicization

- perhaps these governments have used program budgeting effectively

Why does program budgeting not always lead to performance budgeting?

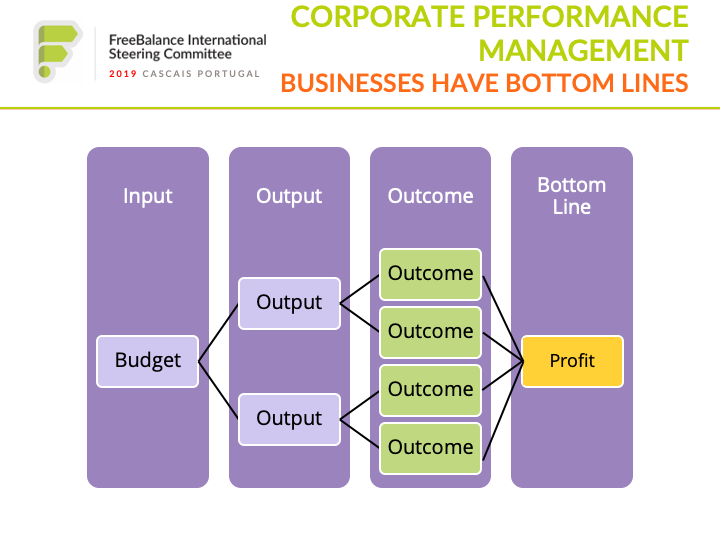

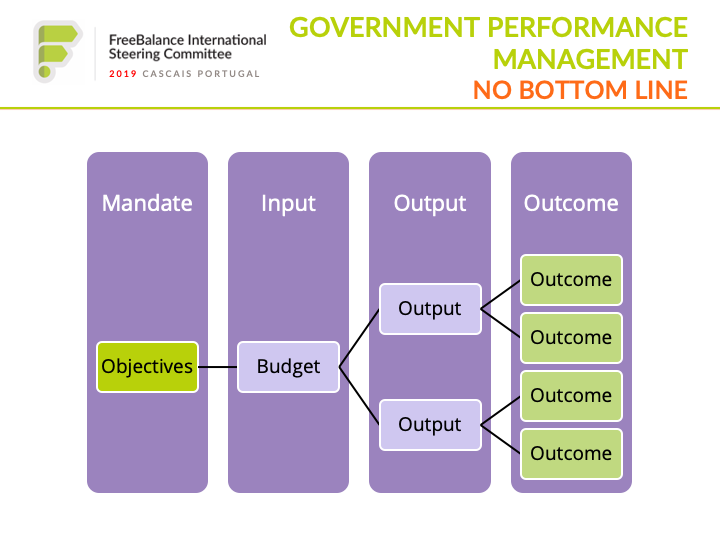

Reality check: performance management is much more difficult in government than in the private sector

- there’s no profit/loss bottom line to validate performance measures and indicators

- outputs are relatively easy to measure, outcomes very difficult because of the time it takes for outcomes (typically beyond a year) and external effects that are outside government influence

Challenges for government performance management include:

- Scope and Scale: Governments run more “lines of business” than any business

- Scope: Governments do not have any definitive bottom line like profit

- Scope: Budgets must be tied to performance because governments run commitment accounting

- Scale: Cascading complex objectives through MDAs and divisions to individual public servants is complex because there are so many staff members

Government performance is more complex than business performance:

- Outcomes are much more difficult to validate in government because is not aligned to an objective bottom line like profit

- Budgets impose more controls on spending in government including restricted flexibility for managers to optimize performance whereas companies can increase spending to generate more revenue or cut costs to reduce expenditures

- Politics drives input-focused (i.e. spending in the politician’s district) decisions that are imposed on public servants

- Financials in the public sector is rarely operating on full accrual accounting, so standard private sector financial measurements like Return on Investment that could help determine effectiveness are difficult to calculate

Meanwhile, there’s a culture of performance as ceremony in some governments, characterized by:

- long imprecise “governmentese” documents rationalizing performance

- lack of splitting outputs from outcomes (vaguely attributing these as “results”)

- complete performance framework changes when new governments come to power

What lessons can governments in developing and developing countries learn?

How can government develop relevant performance structures that adapt to economic shocks and government changes?

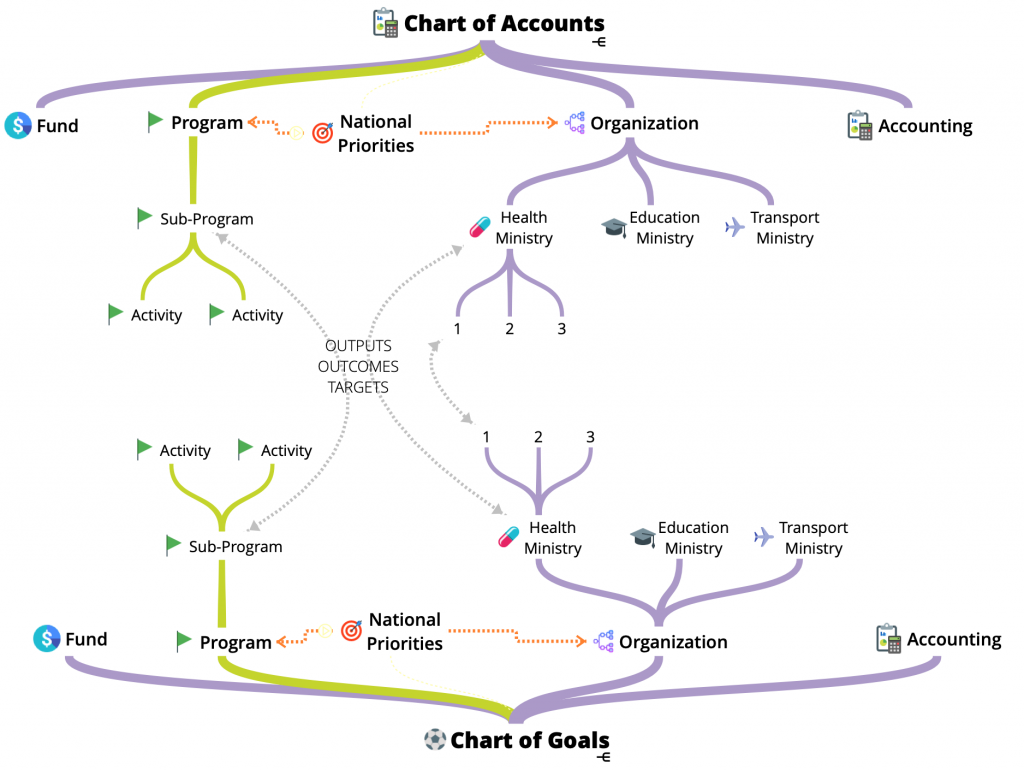

- align spending to national development strategies within budget and accounting classifications

- leverage program budgeting across Ministries, Departments, and Agencies to define spending purposes, rather than separate priority structures

- integrate performance objectives (“Chart of Goals”) with budget and accounting classifications (“Chart of Accounts”)

Why it matters for public finances is the ability to re-allocate for crises response and government changes:

- change spending plans based on priority changes and evidence

- restructure program or performance classifications (if there’s a multiple year COA & COG)

Corporate Performance Management (CPM) is a category of tools including reporting, dashboard, budget and data mining. These are useful tools. Yet, commercial CPM tools designed for the private sector are often missing needed government functionality:

- Budget preparation where performance information is directly tied to the creation of financial budgets and controls

- Forecasting where expenditures are compared with outcomes during the fiscal year to enable performance improvements while ensuring that budgets are not overspent

- Macroeconomic data where key economic information is aligned to the “macro-fiscal” framework and KPIs

- Transparency where government objectives and results are transparently provided to civil society – the kind of information that even publicly-held companies consider business secrets

Other lessons include:

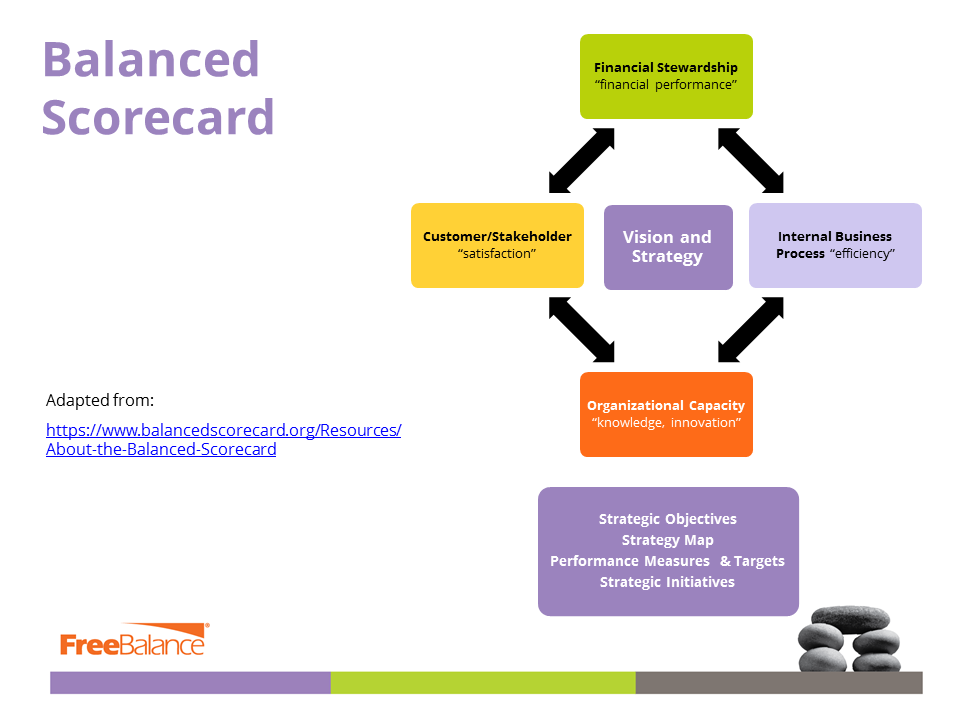

- Private sector practices like Objectives and Key Results (OKRs) and the Balanced Scorecard can be applied in government

- “Positive deviance” is a more effective method to elicit performance concepts than “best practices”

- Multiple methods for effective performance measures

Takeaways: program budgeting is the gateway to performance/results-oriented budgeting

- provides the metadata foundation for performance management

- enables policy and emergency re-allocations

- empowers decision-making based on evidence