Public Finance Innovation is Thriving Globally, Driven by the Covid-19 Crisis!

Learn more about public finance innovation at the upcoming May 4th. International Consortium on Governmental Financial Management webinar: Public Finance Innovation for Sustainable Development: How can finance ministries help governments plan, budget, procure, and manage results in a post-pandemic world

There’s been no lack of Public Financial Management (PFM) advice during the pandemic, but it’s difficult for governments to prioritize reform with so much advice. Where can governments professionals begin to unpack good ideas, and focus on what’s important? We see that the pandemic crisis has exposed opportunities for PFM reform and innovation to enhance disaster resilience:

- Decision-making through integrated fiscal and goal information

- Risk preparedness through planning and governance reform

- Health service delivery through interoperable financial management systems

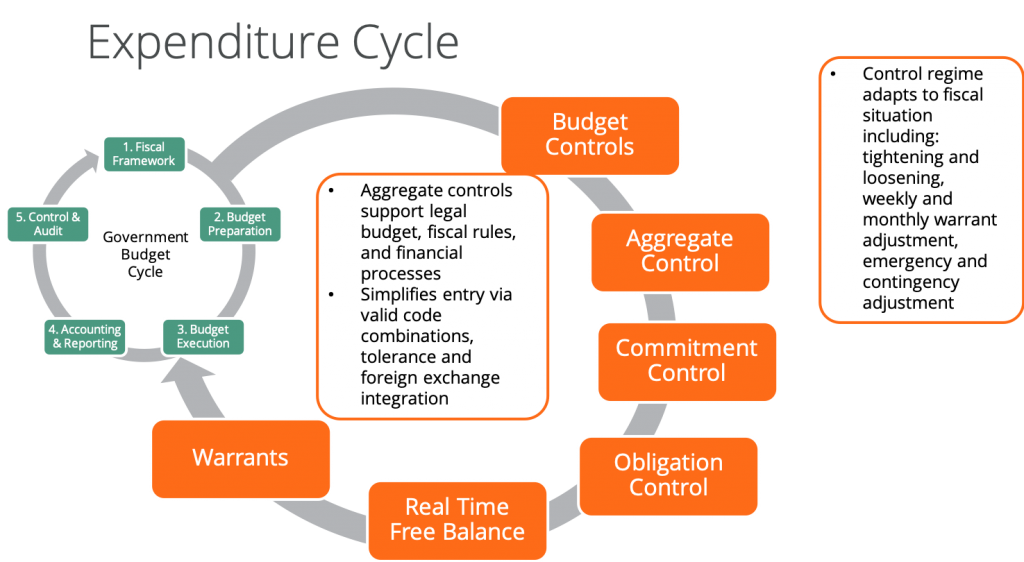

Good PFM systems enable governments to reallocate budgets while temporarily adjusting, loosening, or tightening controls – very temporarily and within reason. This enables accelerating priority pandemic spending. Important PFM spending practices include:

- Clear policy for priority spending and reallocations

- Reoriented rather than diluted controls

- Efficient procurement and payment management

- Expenditure tracking across the budget cycle, including special coding

- Returning to stricter controls post-pandemic

Much like the 2008 financial crisis, the Covid-19 pandemic has coalesced support for PFM reform in many countries. Unlike the previous crisis, the pandemic has motivated innovative approaches in the management of public finances. Are innovative practices used by some governments and many technology firms ready for the mainstream in the public sector?

We see emerging innovation signals among our government customers. We also see a significant unmet need for public finance innovation guidance thanks to our exclusive government focus. That’s why we’ll be sharing our Public Finance Innovation Framework at the upcoming ICGFM webinar. This includes how to effectively use agile techniques, and how to integrate priorities with the Sustainable Development Goals (SDGs).

Reality check is that effective PFM, enabled by underlying systems, has always helped in disaster response for:

- Natural disasters like hurricanes, earthquakes, and tsunamis

- Health crises like pandemics, drought, and food scarcity

- Fragility like rebellion, revolution, and regime change

- Economic shocks like financial crises, trade disputes, and resource price volatility

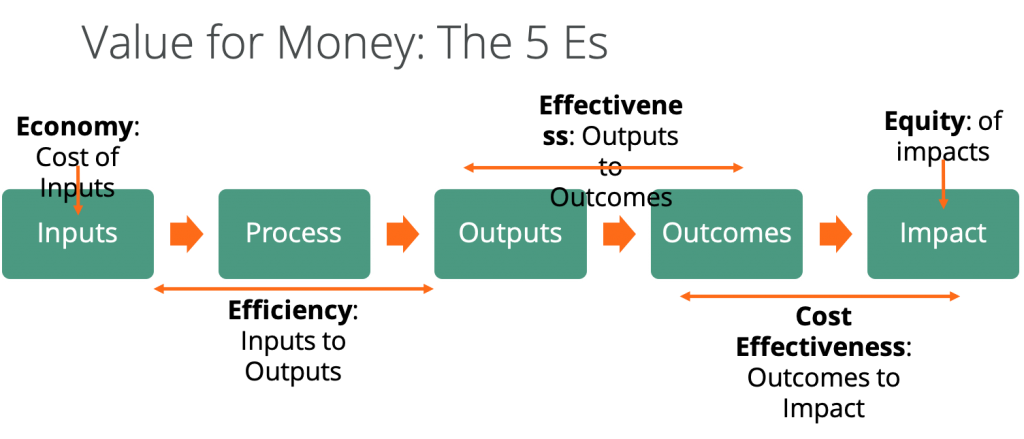

1. Improved Decision-Making

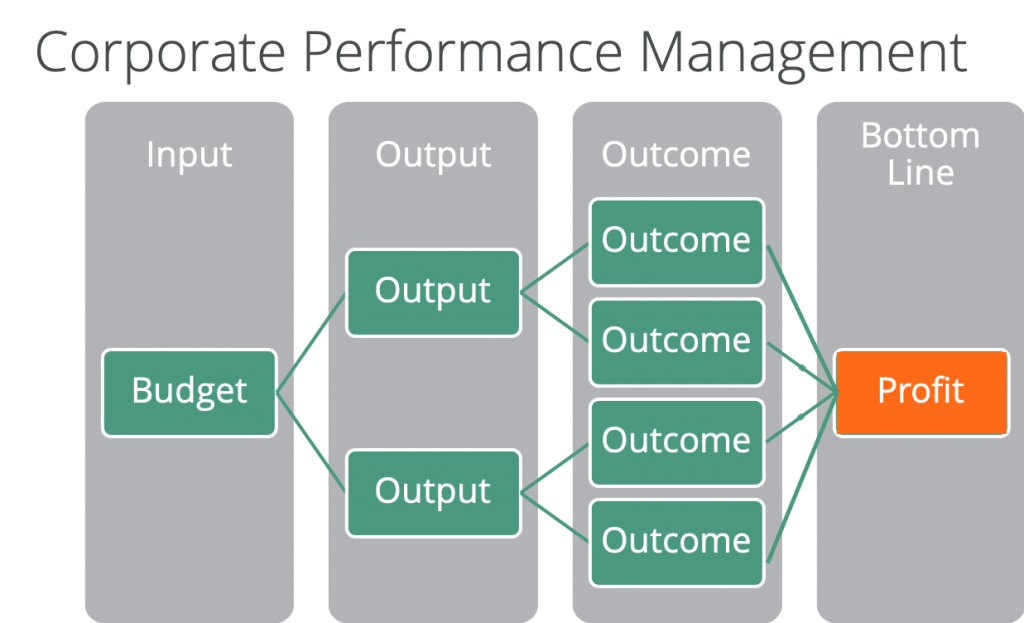

We all know that raw data, complicated reports, and fiscal analysis that is not related to government goals can set decision-making astray. Evidence provided to decision-makers is often late, of low quality, and contradictory to be of value. And, performance management is also more complicated in the public sector than in the private sector. There is no bottom-line of profit and loss in government to validate performance measures.

Performance management concepts are shared between public and private sector organizations, although many businesses do not track “impact”:

- Input: financial and human resources used (for example: cost for malaria vaccines and the share of hospital and clinic costs for administering)

- Process: workflow and procedures used (for example: how malaria vaccines are distributed)

- Output: count of completed procedures (for example: the number of malaria vaccines distributed)

- Outcomes: result of the process (for example: the number of citizens who did and did not contract malaria)

- Impact: contribution to overall citizen improvement (for example: increase in productive days worked and income received thanks to malaria vaccines)

Performance management structures and measures are much easier to validate in the private sector. Businesses decision-makers realize that predominantly meeting output and outcome measures without turning a profit indicates a need to change the scheme. Performance structures in government is much harder to validate. This makes accurate and timely information that much more important in government. As does having a “single version of the truth” across information systems.

This hasn’t stop the trend towards results-based budgeting and other government performance management approaches. There are many hurdles to implementing results-based budgeting:

- Threatens program funding

- Difficultly seeing activities in concert across government silos

- Lack of cascading of national goals to MDAs

- Discover effective measures, rather than use easy measure

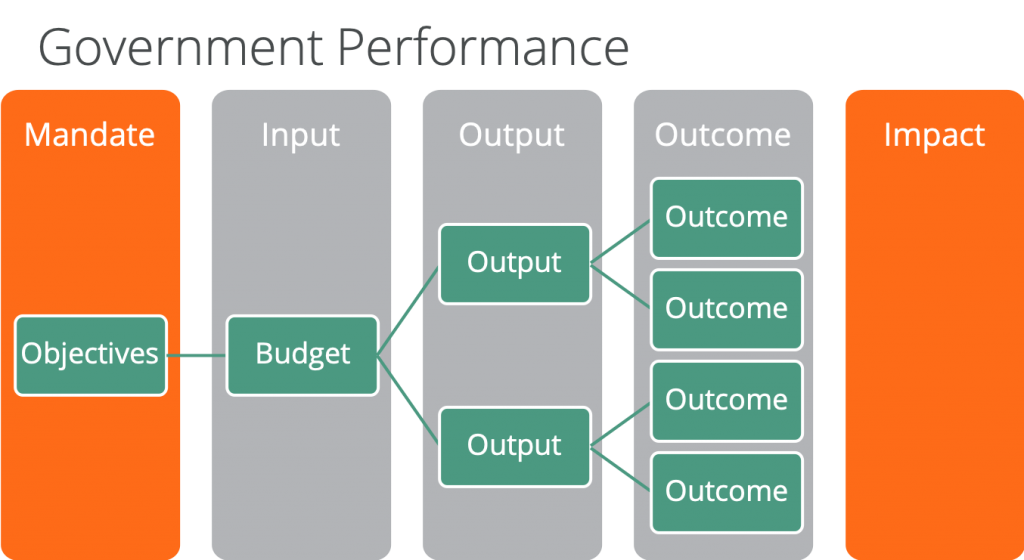

Government performance is more complex than business performance:

- Outcomes are much more difficult to validate in government because is not aligned to an objective bottom line like profit

- Budgets impose more controls on spending in government including restricted flexibility for managers to optimize performance whereas companies can increase spending to generate more revenue or cut costs to reduce expenditures

- Politics drives input-focused (i.e. spending in the politician’s district) decisions that are imposed on public servants

- Financials in the public sector is rarely operating on full accrual accounting, so standard private sector financial measurements like Return on Investment that could help determine effectiveness are difficult to calculate

Meanwhile, there’s a culture of performance as ceremony in some governments, characterized by:

- long imprecise “governmentese” documents rationalizing performance

- lack of splitting outputs from outcomes (vaguely attributing these as “results”)

- complete performance framework changes when new governments come to power

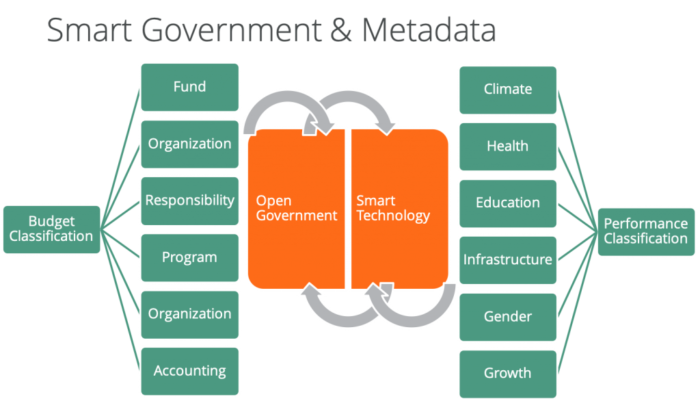

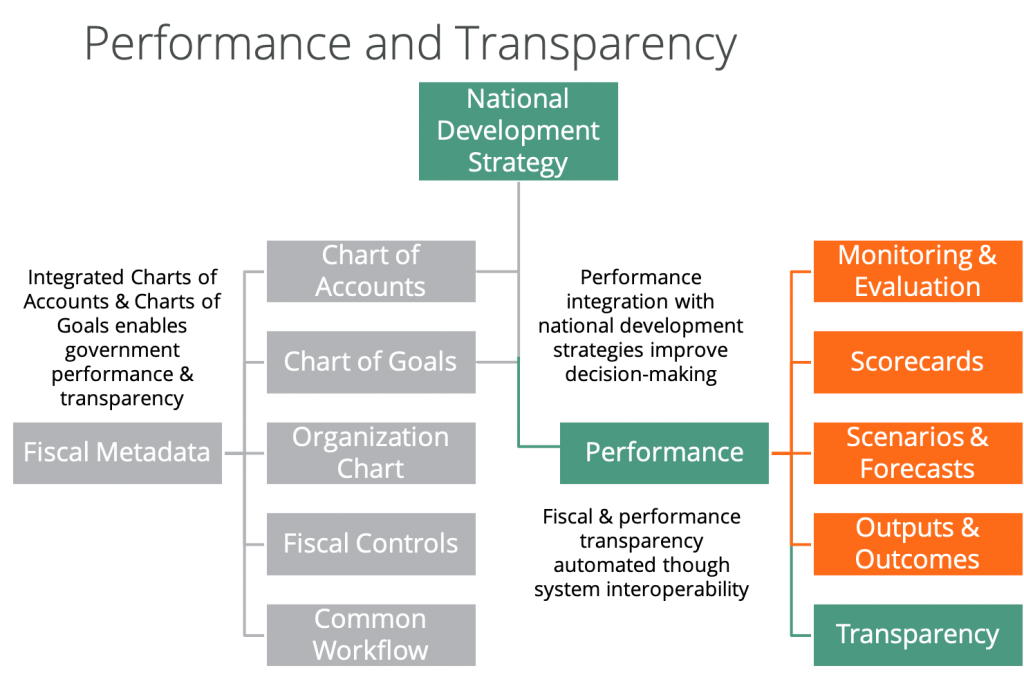

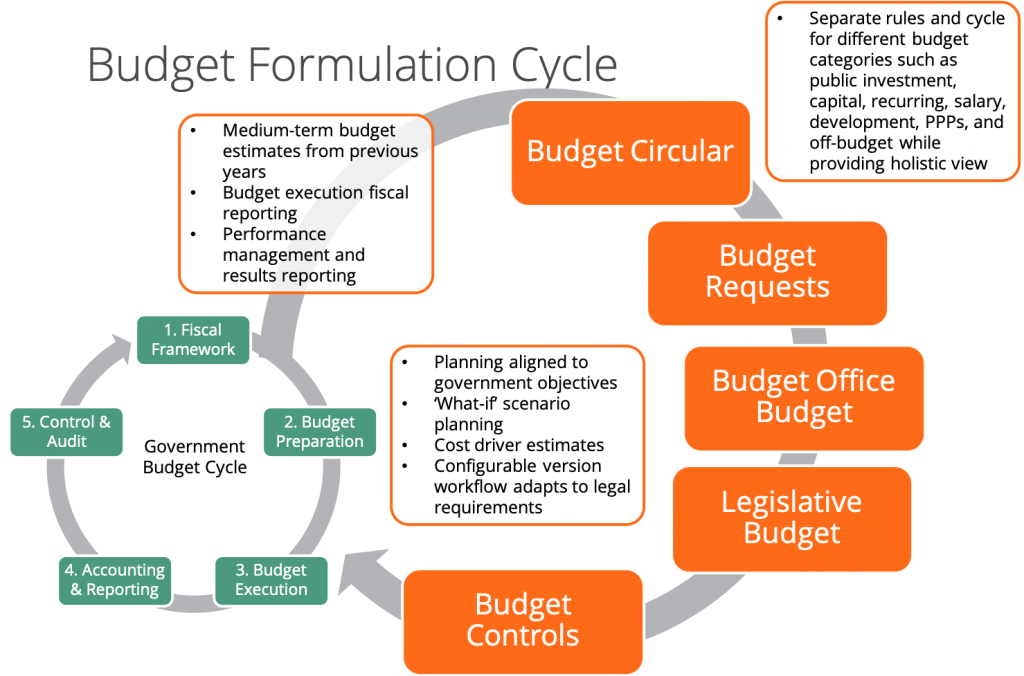

The key to government performance management is integrating budget and accounting classifications with performance classifications. (We call this integrating the Chart of Accounts with the Chart of Goals in the FreeBalance Accountability Suite). Program budgeting is the first step for this by cascading government objectives, like pillars and targets, across MDAs. What’s powerful in program budgeting is the visibility of where MDAs share common objectives. Governments track spending by objectives. This provides decision-making with smart reports and visualization tied directly to what is important.

The other advantage of program budgeting is this linkage with Charts of Goals. The CoG, in the FreeBalance Accountability Suite for example, aligns output and outcome targets to programs. This means that decision-makers are able to evaluate policy outcomes. This approach supports the information integration with national development strategies for performance management and fiscal transparency

Government performance management cascades to specific public finance domains like civil service management and procurement. Individual public servant talent management and performance appraisal can be directly linked to government goals. Value-for-money calculations for complex procurement can also be directly linked to government goals.

Innovation and reform lessons learned:

- Effective decision-making requires integrated, accurate, and timely fiscal evidence

- Program and performance reform provides decision-makers with what is material to policy objectives

- Performance cascades to procurement, human resources, and other public finance functions

- Fiscal transparency to increase citizen trust in government is an attractive byproduct of integration

2. Improved Risk Preparedness

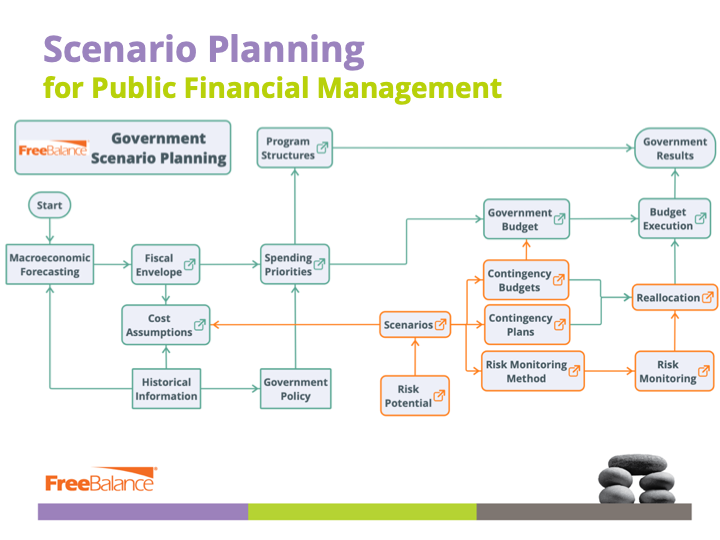

Many observers characterized the pandemic as an unexpected “black swan” event as predicted by the World Economic Forum 2020 Global Risks Report. Although much uncertainty remains, it has become increasingly obvious that governments need to use risk management and contingency budgeting to improve resilience in a Volatile, Uncertain, Complex and Ambiguous (VUCA) world. Risk planning in policy and budget formulation leads to credible fiscal responses to future crisis thanks to effective scenario planning.

{kind=link}

Good scenario planning enables governments to:

- Evaluate the impact of potential crisis on public finances (revenue, debt, expenditures) and citizen service delivery

- Leverage cost assumptions to prepare for reallocations

- Build contingency plans and budgets

- Set up risk monitoring for early warning

Scenario planning is often disconnected from the budget process. Many governments analyze fiscal information in spreadsheets to inform budget circulars. However, most budget projections by Ministries, Departments, and Agencies (MDAs) are accomplished outside of the budget preparation process. There is often no shared cost drivers, financial assumptions, or program integration.

Innovation and reform should be sustainable. Medium-term budget planning is considered a good government practice. We believe that governments should also build medium-term reform plans. These rolling 3 to 5 year plans should provide space for innovation.

Governments have reallocated spending during the pandemic and loosened spending controls to accelerate emergency procurement. This has resulted in corruption incidents from advanced economies to developing countries. These types of risks are well-understood in the PFM community.

Governments can reduce expenditure corruption risk by:

- Maintaining segregation of duties in procurement decisions

- Loosening controls temporarily while tracking each stage of the expenditure cycle

- Leveraging valid code combinations and developing specific emergency accounting codes to ensure that only authorized government entities are spending

- Analyze spending by leveraging audit trails

- Fully interoperable procurement and financial systems so that all acquisitions are compliant with controls

Governments are often unable to maintain a needed trajectory and cadence for PFM reform. Medium-Term Sustainability Planning can overcome:

- Lack of progress from reform fatigue or attempting to consume more reform than is reasonable in the government circumstances

- Push reform from international donors that might not be appropriate for the government circumstances

- Country system bypassed by international donors that limits progress for one of the most important outcomes from PFM reform = budget, spending, and results integration by leveraging country systems

- Poor sequencing of PFM reform based on international assessments rather than what is appropriate for the government context

- Technology limitations that make legitimate reform difficult because of highly customized code bases that were not designed for multiple modernization phases

Fiscal risk reporting is a new Public Expenditure and Financial Accountability (PEFA) metric in the 2016 framework. The new PI-10 is part of the Management of Assets and Liabilities. PEFA identifies the need for performance information integration: “effective management of assets and liabilities ensures that public investments provide value for money, assets are recorded and managed, fiscal risks are identified, and debts and guarantees are prudently planned, approved, and monitored.”

Innovation and reform lessons learned:

- World Economic Forum and other sources of risk information enables effective scenario planning and risk preparedness

- PFM modernization for risk management focuses on improving the fiscal framework and budget formulation stages of the government budget cycle

- Governance mechanism may be needed to effectively plan and monitor risks

- Integration of financial management sub-systems, like procurement, with core Financial Management Information Systems (FMIS), to maintain controls, with up-to-date reporting, even in emergencies

- Use of a medium-term approach to PFM and GRP sustainability to sequence modernization while uncovering opportunities for innovation

3. Improved health service delivery

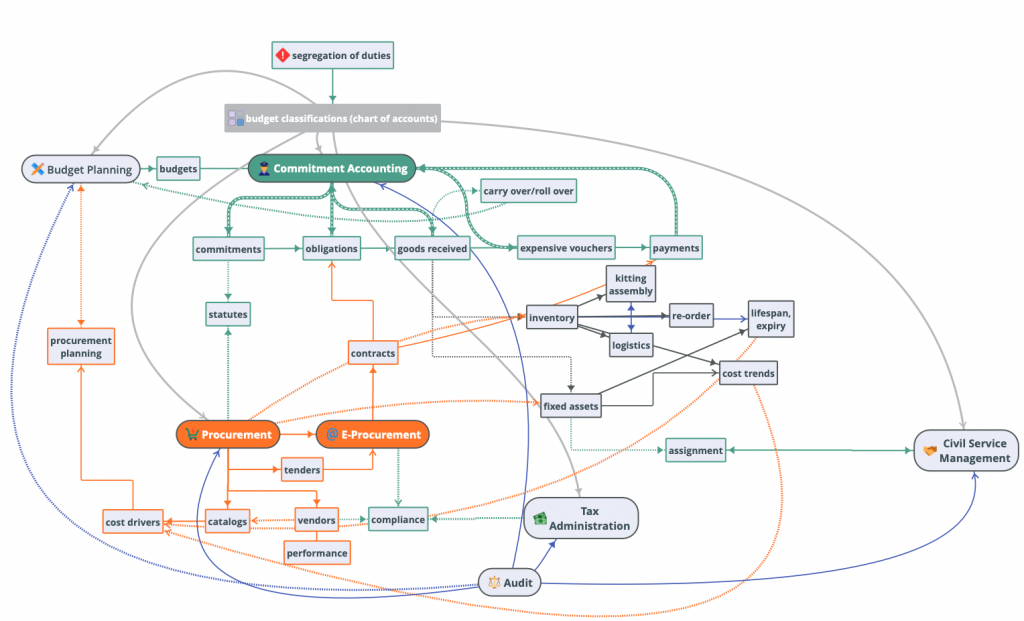

Governments have struggled with health procurement and service delivery during the pandemic. It seems like for every success story, there’s a handful of fail stories. What is often misunderstood is how public finance functions enhance emergency response. Governments have been faced with a lack of interoperability among financial informations systems – what we call Government Resource Planning (GRP). A significant inhibitor to supporting effective health responses comes from the lack of integration between Electronic Government Procurement (e-GP) and core Financial Management Information Systems (FMIS). Among the problems experienced include some elements described in the previous section:

- Corruption because of the lack of controls on segregation of duties integration

- Inability to track health procurement from requisition through consumption

- Reallocation confusion when pandemic priority changes were not reflected across information systems

Effective PFM systems interoperate to support:

- Credible procurement planning based on tender results and vendor catalogs

- Compliant and automated health procurement through integration with metadata, controls, and segregation of duties from commitment accounting and tax administration system

- Automated tracking of health inventory and assets, including responsibility assignments with human resource systems

The pandemic has reduced trust in government fiscal and health response. Transparency, enabled by interoperability, can improve trust. For example, many governments publish monthly PDFs. Do citizens trust these static documents? A more effective method is to provide the ability for citizens to drill into procurement information showing pandemic:

- Budget allocations

- Procurement processes

- Purchase orders, prices, and winning bidders

- Location of relevant inventory and assets

- Consumption of health inventory

Some innovation ideas for health resilience include:

- Improving strategic spending for health procurement though spend aggregation, framework agreements, and agile procurement

- Treating health as a social public investment by integrating capital and operating budgets

- Identifying health outputs and outcome measurements

Innovation and reform lessons learned:

- Interoperability among information systems is required for effective crisis response particularly for controls and tracking acquisitions

- Fiscal transparency for crisis response is also enabled through interoperable systems

- Standalone e-procurement systems prevent needed interoperability

FreeBalance Accountability Suite approach

Governments leverage different Financial Management Information Systems to support emergency spending and planning. The FreeBalance Accountability Suite supports:

Budget and Risk Planning

- Leverage cost drivers to support scenario planning and set cost assumptions

- Integrate policy to planning through program and performance budgeting

- Use multiple-year perspectives to support MTEF and provide information trends

- Support multiple scenario plans using subsets of information that can be triggered during budget execution modelled with new actual information

- Support multiple versions of budget plans that can also be analyzed during a crises

Budget reallocations

- Configure new budget classifications, including support for programs, to enable reallocation

- Increase budgets for pandemic spending purposes through budget transfers based on budget classifications

- Decrease spending for lower priorities through budget transfers

- Empower decentralization of budget transfers to pandemic spending

- Leverage program budgeting (in the multiple-year Chart of Accounts design) to better understand impact of any budget transfers on government priorities

Control changes

- Configure commitment controls & levels of aggregation temporarily for pandemic spending

- Accelerate approvals for pandemic spending through escalation to more decision-makers

Track spending

- Configure fund source in budget classifications to track the entire pandemic cycle

- Forecast spending needs based on trends

- Improve decision-making through integration of commitments, procurement, assets and inventory

- Demonstrate progress by tracking in-progress commitments and purchase orders

- Track outputs like medical supplies and assets, including consumption

- Create fiscal transparency portals to gain citizen and donor trust

Interoperability

- Unified design where underlying components are shared among all FreeBalance applications

- Single point for controls, workflow, and metadata changes

- Single version of the truth for timely decision-making and fiscal transparency

Post Pandemic Innovation and Reform

How can governments improve fiscal resilience for crises? Governments can modernize fiscal management in a phased approach aligned to the PFM context:

- Horizon 1: improve selected processes by tweaking current technology investments and increasing automation of decision-making and fiscal transparency information during the pandemic

- Horizon 2: leverage risk and opportunity analysis to improve additional processes and integration for the post-pandemic recovery period

- Horizon 3: use an integrated analysis approach to identify biggest impact from technology modernization, process and legal reform

Horizon 2 is particularly useful for uncovering innovation opportunities to modernize government processes and technology. Horizons 2 and 3 can be informed by government commitments to support the SDGs, the focus of the upcoming ICGFM webinar.