…as Long as it’s not Overwhelming!

Second post of 3 in a series, PFM takeaways from 2020

- 2020 The Year that PFM Came in from the Cold

- Overwhelming motivation for PFM reform in 2021/2022

- PFM and the Volatile, Uncertain, Complex & Ambiguous World

It’s a bit difficult to unpack all the Public Financial Management (PFM) advice given to governments since March 2020 – an information overload. The pandemic exposed the best and the worst of PFM. You could get the impression that governments should immediately adopt “best practices” of:

- Full accrual accounting

- Result-based budgeting and performance management

- Multiple year expenditure frameworks

- International public sector standards support

That’s not to say that effective PFM results in stellar government performance during the pandemic. PFM can’t tell policy-makers about the health and economic impact of:

- Lockdowns

- Vaccines

- Existing medicines

- Masks and “social distancing”

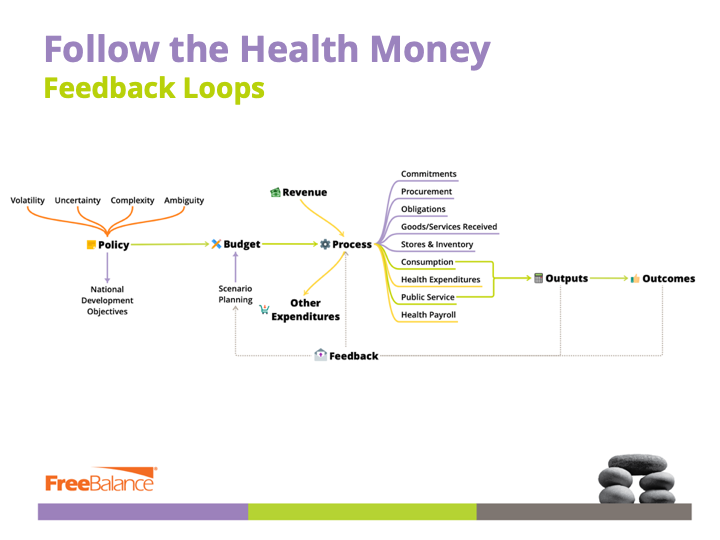

Effective PFM helps governments follow the money. It helps governments to adjust spending priorities as health and economic outcomes are realized. It does help to improve service delivery during the pandemic period – that’s the important and immediate integration point.

What are the big PFM lessons for governments from 2020? PFM is core to good governance and:

- Trust

- Trust

- Trust

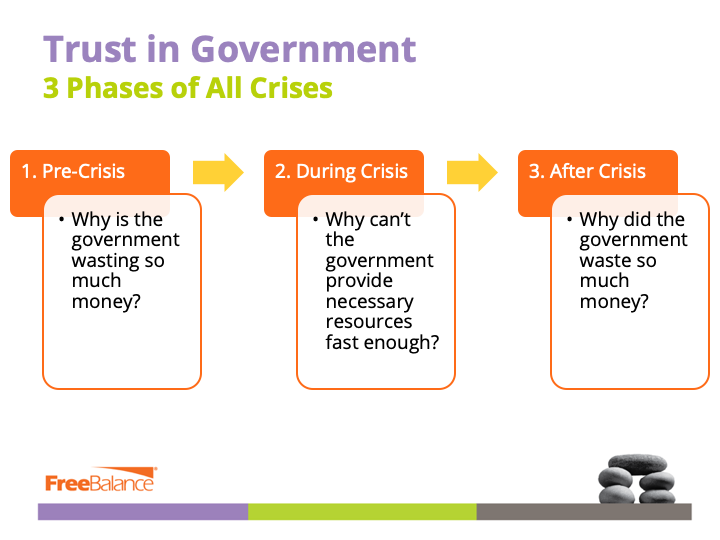

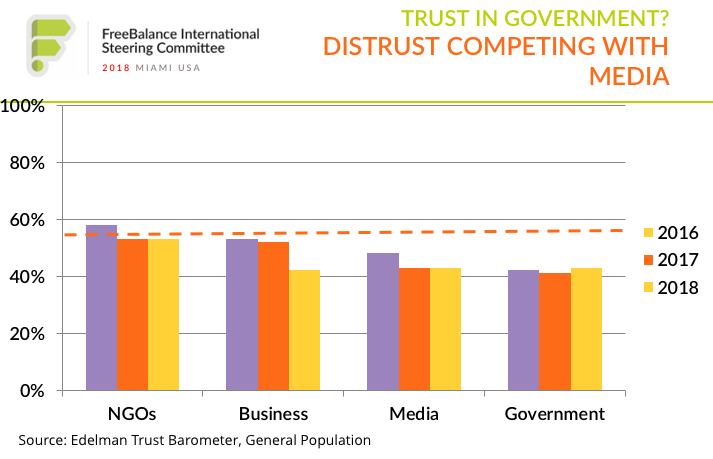

Poor government health and economic response generates distrust. Poor stewardship and transparency of public funds is a distrust force multiplier.

- Citizens recognize that corruption thrives when procurement procedures are accelerated, controls are loosened, and where fiscal transparency is lacking.

An alternative view: more transparency results in more distrust. Not in the long-run! Our planet is in the midst of a “fake news” pandemic – the “infodemic”. There’s no end to the imagination of people not blessed with timely and accurate government information.

Reform lesson: “best practices” aren’t “best”- “perfect is the enemy of good”

Best practices without transparency results in no trust, good practices with transparency makes for public trust. And, trust encourages future reform. PFM excellence is a journey, not a destination.

What’s the PFM reform problem with “best practices”?

- Many so-called “best practices” are not “best” or appropriate based on the government context

- Human capacity, perverse incentives, and politics affects reform decisions and slows legal reform

- Many advanced countries have yet to adopt many “best practices” demonstrating the difficulty of adopting in government

That’s not to say that governments should not consider advanced practices.

Take: accrual accounting following International Public Sector Accounting Standards. Would a government following these standards have managed pandemic spending better? Would the government have been more fiscally transparent?

- Spending could be effectively tracked using commitment accounting in a cash-based system (showing budget reallocation, requisitions, purchase orders, goods received, total spending)

- Spending transparency can be supported across the commitment cycle

- PPE inventory and medical assets can be tracked without the use of accrual accounting

- Debt, revenue, and other expenditures like wage bills can all be tracked by Financial Management Information Systems

In other words, the use of accrual accounting without integration among financial systems reduces the quality and timeliness of decision-making and fiscal transparency information. Whereas, integration in a cash-based accounting method improves information quality and timeliness.

That’s not to say that accrual or modified accrual accounting does not provide PFM benefits. For one thing, arrears are more visible and appear on financial statements.

Public Financial Management reform momentum

The consensus: the pandemic crisis will motivate PFM reform and overcome change resistance. My view is that appetite might overwhelm capacity. As the saying goes: “don’t waste a perfectly good crisis”. Look at it strategically:

- Determine reform priorities based on the government context by analyzing what worked and what didn’t work in the government PFM pandemic response

- Identify which recommended practices will improve the government response to the next crisis – not necessarily “best practices”, but certainly not “poor practices”

- Progressively activate reform across 3 time horizons:

- what can be immediately improved during the pandemic

- what can be implemented in the post-pandemic period

- what needs legal reform, significant change management and capacity building

Sample PFM Reform Strategy

This is an example of an optimistic approach to reform across 3 Horizons. Many reforms listed in the table should be in “Horizon 4” in many countries.

Yes, FreeBalance provides a set of services to help governments map PFM reform strategies across time frames based on context. You can find out more by requesting a call at info@freebalance.com.

| Horizon 1: During Pandemic Action | Horizon 2: Post-Pandemic Reform | Horizon 3: Sustaining Reform |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

How does PFM improve trust in government?

{kind=link}

PFM reform improves trust through:

- Service Delivery: budgets aligned to citizen needs to deliver what is most valued

- Fiscal Transparency: plans, debt, revenue, and expenditure transparency to demonstrate the priorities and performance for using public money

- Anti-Corruption: segregation of duties and fiscal controls augmented by citizen audit and independent anti-corruption organizations

- Audit: internal and external audit for compliance and performance improvements